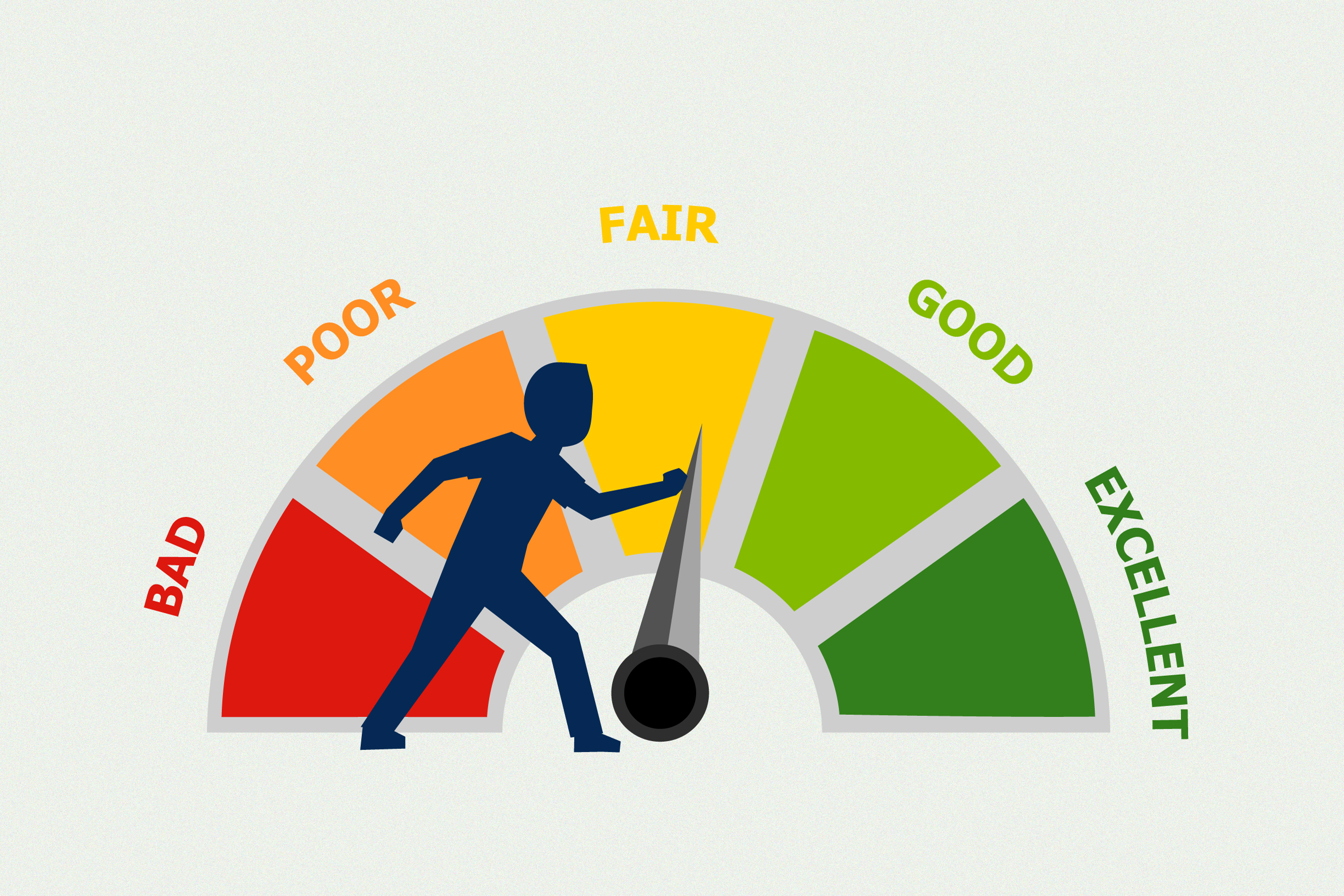

Finance

Is your loan getting refused? Best ways to improve your credit score

Your credit score is a three-digit figure that represents your borrowing worthiness. Do you repay your loans on time? Have you used a substantial quantity of credit in your financial history? Is there a good chance you’ll fall behind on your payments? Your credit score provides answers to these queries. When you ask for a loan, lenders such as banks and financial institutions examine your credit score and credit profile before approving your application. Your credit score not only determines your ability to borrow, but it also affects the interest rate you will be paid. This is especially true for small Personal Loans and fast loans, for which no collateral is required.

Limit difficult enquiries

When you apply for a loan, a potential lender will conduct a hard investigation as one of the initial steps. The lender examines your credit report to evaluate whether to approve you. A hard inquiry has a minor negative impact on your credit score because it momentarily lowers your ranking. So, before you formally apply for modest Personal Loans, fast loans, or other types of borrowings, do your homework. You don’t want to risk a harsh enquiry for a potentially declined application.

Make your EMI payments on time

If you have additional debts, make sure you pay your Equated Monthly Instalments (EMIs) on time. Repayments have a big impact on your credit score. If your credit history reveals that you were not extremely attentive about repaying your loans on time, it may affect your future borrowing potential. Even if you successfully repay your existing loans before applying for a new one, your history of late EMI payments will remain on your credit report.

Reduce your credit utilisation ratio

At any one time, your credit utilisation rate is computed by dividing the amount you owe your lenders (in loans and credit card payments) by your entire credit limit. The lower this proportion, the higher your credit score. It is preferable to have a credit utilisation ratio of 30% or below. A low ratio suggests that you are adept at credit management. Avoiding credit card debt is one strategy to improve your credit utilisation percentage. Another thing you may do is pay off your debts as soon as possible.

Make on-time payments on your utility bills

Your payment history for utility bills has an impact on your credit score. If you put off paying your phone bills, internet bills, and other utility bills until you receive a reminder, you are jeopardising your credit score. Set up phone reminders to remain on top of your monthly utility and cell phone bills. Even if you use apps that allow you to use services right immediately and pay later, you must assure fast payment before the deadline.

Keep a healthy credit mix

Your credit portfolio should include a healthy balance of secured and unsecured borrowings, as well as long-term and short-term obligations. If you’ve taken out too many huge loans in the past, opt for small Personal Loans or fast loans in the future if you need to cover an unexpected need. Alternatively, if you have never borrowed money before, you will not have a credit history. You can start building a credit profile by obtaining a credit card to finance your routine expenditures. To avoid poor credit ratings, make sure you pay your credit card bills on time.

Avoid taking on too much debt at once

Taking on too much debt in a short period of time is not the best way to improve your credit score. It may work against you and harm your credit score. Taking out many loans will indicate to a potential lender that you are trapped in a never-ending cycle of insufficient finances. It also implies that you are already swamped with EMIs to repay, making it difficult to obtain a new loan. The ideal course of action is to obtain one loan, repay it completely, and then consider borrowing again if necessary.

You may increase your credit score in the long run by incorporating these behaviours into your spending pattern and following these guidelines. This makes obtaining a loan later in life easier. Another option you can use to boost your credit score and creditworthiness is Bajaj Finserv’s credit builder programme. And, once you’ve reached a healthy credit score, keep in mind that the same habits that helped you build your credit profile will help you keep it. Apply for loan at Bajaj Finserv today.

Introduction

Jeff Carriveau has built a reputation as a skilled professional whose career achievements have sparked curiosity about his financial success. While exact figures remain private, understanding his professional journey and accomplishments provides insight into how he has accumulated wealth over the years.

Carriveau’s name frequently appears in discussions about successful business professionals, leading many to wonder about the financial rewards of his career path. His strategic decisions and professional expertise have positioned him as a notable figure worth examining from both career and financial perspectives.

This analysis explores the various factors that have contributed to jeff carriveau net worth examining his career trajectory, business ventures, and the methods typically used to calculate such financial assessments.

Professional Background and Career Highlights

Jeff Carriveau’s professional journey spans multiple industries and roles, each contributing to his overall financial portfolio. His career demonstrates a pattern of strategic positioning and calculated moves that have enhanced his earning potential.

Throughout his professional life, Carriveau has shown an ability to identify opportunities and capitalize on them effectively. His background includes roles that have provided both immediate compensation and long-term financial benefits, creating multiple income streams that contribute to his overall wealth.

The diversity of his professional experiences has allowed him to develop expertise in various areas, making him valuable in different markets and increasing his earning potential across multiple sectors.

Factors Contributing to Financial Success

Several key elements have played a role in building Jeff Carriveau’s financial foundation. His approach to career development shows a clear understanding of how to maximize earning potential while building sustainable wealth.

Strategic Career Positioning

Carriveau’s ability to position himself in high-value roles has been crucial to his financial growth. By focusing on positions that offer both competitive compensation and growth opportunities, he has created a solid foundation for wealth accumulation.

His professional network and reputation have opened doors to lucrative opportunities that might not be available to others in similar fields. This strategic networking has proven valuable in securing positions and partnerships that contribute significantly to his net worth.

Multiple Revenue Streams

Like many successful professionals, Carriveau appears to have diversified his income sources beyond traditional employment. This diversification strategy helps protect against economic downturns while maximizing earning potential during favorable market conditions.

His involvement in various projects and ventures suggests an understanding of the importance of not relying on a single income source, a principle that has likely contributed significantly to his overall financial success.

Understanding Net Worth Calculations

Net worth calculations involve assessing all assets and subtracting any liabilities to determine an individual’s total financial position. For public figures like Jeff Carriveau, these calculations often rely on publicly available information and educated estimates.

Assets typically include real estate holdings, investment portfolios, business interests, and liquid assets such as cash and savings accounts. Professional achievements and ongoing projects can also indicate potential asset values and future earning capacity.

Liabilities might include mortgages, business loans, and other debts that reduce the overall net worth figure. However, successful professionals often structure their finances to minimize liabilities while maximizing asset growth.

The challenge with calculating net worth for private individuals lies in the limited availability of specific financial information, requiring analysts to make educated estimates based on career achievements, lifestyle indicators, and industry standards.

Estimated Net Worth Range

Based on available information about Jeff Carriveau’s career achievements and professional standing, financial analysts estimate his net worth to fall within a substantial range. These estimates consider his career trajectory, industry standards for similar professionals, and observable lifestyle factors.

While exact figures remain confidential, his professional accomplishments suggest a net worth that reflects years of strategic career building and smart financial decisions. The estimate takes into account both his current assets and ongoing earning potential from various professional endeavors.

These calculations also consider the typical wealth accumulation patterns of professionals in similar positions, providing context for understanding how Carriveau’s financial success compares to industry peers.

It’s important to note that net worth estimates for private individuals are inherently speculative and should be viewed as approximations rather than precise calculations.

Future Financial Prospects

Jeff Carriveau’s current projects and professional positioning suggest continued potential for financial growth. His established reputation and ongoing ventures indicate that his net worth may continue to increase in the coming years.

The sustainability of his income streams and his strategic approach to career development provide a strong foundation for future wealth accumulation. His ability to adapt to changing market conditions and identify new opportunities will likely influence his long-term financial trajectory.

Market conditions, industry trends, and personal financial decisions will all play roles in determining how his net worth evolves over time. However, his track record suggests a strong likelihood of continued financial success.

Building Wealth Through Professional Excellence

Jeff Carriveau’s financial success story illustrates the potential rewards of strategic career planning and professional excellence. His journey demonstrates how focused effort, smart positioning, and diversified income streams can contribute to substantial wealth accumulation over time.

While specific figures may remain private, his professional achievements provide valuable insights into the financial benefits of building expertise, maintaining strong professional relationships, and continuously seeking growth opportunities.

For those looking to understand wealth building in professional contexts, Carriveau’s approach offers practical lessons about the importance of strategic thinking, network building, and maintaining multiple income sources.

Frequently Asked Questions

What is Jeff Carriveau’s exact net worth?

Jeff Carriveau’s exact net worth is not publicly disclosed. Estimates are based on his professional achievements and industry standards, but specific figures remain private.

How did Jeff Carriveau build his wealth?

Carriveau built his wealth through strategic career positioning, multiple income streams, and professional expertise developed across various industries and roles.

What industries has Jeff Carriveau worked in?

While specific details vary, Carriveau has demonstrated expertise across multiple sectors, contributing to his diverse professional portfolio and financial success.

Is Jeff Carriveau’s net worth likely to grow?

Based on his current projects and professional trajectory, continued financial growth appears likely, though market conditions and personal decisions will influence future outcomes.

How reliable are net worth estimates for private individuals?

Net worth estimates for private individuals like jeff carriveau net worth are approximations based on available information and should be viewed as educated guesses rather than precise figures.

Introduction

The financial trading landscape has transformed dramatically over the past decade, with retail investors gaining unprecedented access to global markets. Among the platforms emerging to serve this growing community, EverestEx has positioned itself as a comprehensive solution for both novice and experienced traders seeking to navigate the complexities of modern financial markets.

EverestEx operates as a multi-asset trading platform, providing users with access to stocks, forex, commodities, cryptocurrencies, and other financial instruments through a single interface. The platform combines traditional trading capabilities with modern technology, offering tools designed to help traders make informed decisions while managing risk effectively.

This comprehensive guide explores everything you need to know about the EverestEx trading platform, from its core features to advanced strategies that can help maximize your trading potential. Whether you’re taking your first steps into trading or looking to enhance your existing approach, understanding what EverestEx offers can help you make better-informed decisions about your financial future.

Key Features and Benefits

Multi-Asset Trading Capabilities

EverestEx distinguishes itself by offering access to diverse financial markets through a unified platform. Traders can execute transactions across equity markets, foreign exchange, commodities, and digital assets without needing to maintain multiple accounts with different brokers.

The platform’s asset coverage includes major stock exchanges, providing access to blue-chip companies and emerging market opportunities. Currency pairs span major, minor, and exotic combinations, while commodity trading encompasses precious metals, energy products, and agricultural futures.

Advanced Charting and Analysis Tools

Technical analysis forms the backbone of many successful trading strategies, and EverestEx provides comprehensive charting capabilities to support this approach. The platform includes multiple chart types, from traditional candlestick patterns to specialized indicators that help identify market trends and potential entry points.

Real-time data feeds ensure that traders have access to current market information, while historical data allows for backtesting strategies and understanding long-term market behavior. Custom indicators can be created and saved, enabling traders to develop personalized analysis methods.

Risk Management Systems

Effective risk management often determines the difference between profitable and losing traders. EverestEx incorporates several risk management tools designed to help protect trading capital and minimize potential losses.

Stop-loss orders can be set automatically, closing positions when predetermined loss thresholds are reached. Take-profit orders work similarly for locking in gains. Position sizing calculators help determine appropriate trade sizes based on account balance and risk tolerance.

How to Get Started

Account Registration Process

Beginning your journey with EverestEx starts with creating an account through their registration system. The process typically involves providing basic personal information, verifying your identity through documentation, and completing any required financial assessments.

Account verification helps ensure platform security and compliance with financial regulations. This step usually requires submitting government-issued identification and proof of address. The verification process may take several business days to complete.

Initial Deposit and Funding Options

Once your account is verified, funding becomes the next step. EverestEx typically supports multiple deposit methods, including bank transfers, credit cards, and electronic payment systems. Minimum deposit requirements vary based on account type and jurisdiction.

Understanding fee structures for deposits and withdrawals helps avoid unexpected costs. Some payment methods may incur processing fees or take longer to clear, so reviewing available options before making your first deposit can save time and money.

Platform Navigation and Setup

Familiarizing yourself with the platform interface before placing live trades can prevent costly mistakes. EverestEx usually offers demo accounts that allow practice trading with virtual funds, providing an opportunity to explore features without financial risk.

Customizing the workspace to match your trading style improves efficiency. This might include arranging chart layouts, setting up watchlists for frequently monitored assets, and configuring alert systems for price movements or news events.

Trading Strategies

Fundamental Analysis Approach

Fundamental analysis involves evaluating assets based on economic factors, company performance, and market conditions. EverestEx typically provides access to news feeds, economic calendars, and financial reports that support this analytical approach.

Economic indicators such as employment data, inflation rates, and central bank policies can significantly impact asset prices. Understanding how to interpret and apply this information helps traders make decisions based on underlying market forces rather than just price movements.

Technical Analysis Methods

Technical analysis focuses on price patterns and statistical indicators to predict future market movements. The EverestEx platform’s charting tools support various technical analysis methods, from simple moving averages to complex oscillators and momentum indicators.

Common technical strategies include trend following, where traders identify and follow established market directions, and mean reversion, which involves trading against short-term price movements with the expectation that prices will return to average levels.

Risk-Reward Optimization

Successful trading often requires maintaining positive risk-reward ratios, where potential profits exceed potential losses on each trade. This approach helps ensure profitability even when some trades result in losses.

Position sizing plays a crucial role in risk management. Rather than risking the same dollar amount on every trade, many successful traders risk a consistent percentage of their account balance, typically between 1-3% per trade.

Advanced Tools and Resources

Automated Trading Features

For traders seeking to implement systematic approaches, EverestEx may offer automated trading capabilities. These tools allow users to create rules-based strategies that execute trades without manual intervention.

Automated systems can help remove emotional decision-making from trading while ensuring consistent application of predetermined strategies. However, these systems require careful testing and monitoring to ensure they perform as expected under various market conditions.

Market Research and Analytics

Access to professional-grade research can significantly enhance trading decisions. EverestEx typically provides market analysis, research reports, and expert commentary to help traders understand current market conditions and potential opportunities.

Regular market updates help traders stay informed about factors that might impact their positions, from geopolitical events to corporate earnings announcements and economic policy changes.

Educational Resources

Continuous learning remains essential for trading success, particularly as markets evolve and new opportunities emerge. Educational materials might include webinars, tutorials, and comprehensive guides covering various aspects of trading and market analysis.

Understanding different market sectors, trading psychology, and advanced strategies can help traders develop more sophisticated approaches to market participation.

Community and Support

Customer Service and Technical Support

Reliable customer support becomes crucial when technical issues arise or questions need immediate answers. EverestEx typically offers multiple support channels, including live chat, phone support, and email assistance.

Response times and support quality can significantly impact the trading experience, particularly during volatile market periods when quick resolution of issues becomes essential.

Trading Community and Forums

Many platforms foster trader communities where users can share insights, discuss strategies, and learn from each other’s experiences. These communities can provide valuable perspectives and help newer traders learn from more experienced participants.

However, it’s important to remember that trading advice from community members should be carefully evaluated and never followed blindly, as individual circumstances and risk tolerances vary significantly.

Frequently Asked Questions

What are the minimum deposit requirements for EverestEx?

Minimum deposit requirements typically vary based on account type and geographic location. Most platforms offer different account tiers with varying minimum deposits, starting from as low as $100 for basic accounts and increasing for premium accounts with additional features.

Does EverestEx offer demo accounts for practice trading?

Most reputable trading platforms, including EverestEx, typically provide demo accounts that allow users to practice trading with virtual funds. These accounts help new traders familiarize themselves with the platform and test strategies without risking real money.

What markets and assets are available for trading?

EverestEx typically offers access to multiple asset classes, including stocks, forex pairs, commodities, and potentially cryptocurrencies. The specific instruments available may vary based on regulatory requirements in different jurisdictions.

Are there educational resources available for new traders?

Educational resources are commonly provided by trading platforms to help users improve their skills. These might include video tutorials, webinars, trading guides, and market analysis to support both beginners and experienced traders.

How does EverestEx ensure the security of user funds and data?

Reputable trading platforms implement multiple security measures, including encryption, segregated client accounts, and regulatory compliance. Users should verify that their chosen platform maintains appropriate licenses and follows industry security standards.

Taking Your Next Steps in Trading

EverestEx represents one of many platforms available to modern traders seeking access to global financial markets. Success in trading depends not just on platform selection, but on developing sound strategies, maintaining disciplined risk management, and continuously educating yourself about market dynamics.

Before committing significant capital, take advantage of educational resources and demo accounts to build your skills and confidence. Remember that trading involves substantial risk, and it’s possible to lose more than your initial investment, particularly when using leverage.

Consider starting with smaller positions while you develop your trading approach, and never invest more than you can afford to lose. The most successful traders often emphasize patience, discipline, and continuous learning over quick profits.

Whether EverestEx becomes your platform of choice or you explore other options, the key to long-term success lies in understanding the markets, managing risk effectively, and maintaining realistic expectations about trading outcomes.

Introduction

Converting numbers to their written form might seem straightforward, but “numero a letras” (number to letters) conversion involves more complexity than most people realize. Whether you’re writing formal documents, creating legal contracts, or ensuring accessibility compliance, knowing how to accurately transform numerical values into their textual equivalents is an essential skill.

This comprehensive guide will walk you through everything you need to know about numero a letras conversion. You’ll discover practical tools, learn manual techniques, and understand best practices that ensure your number-to-text conversions are always accurate and professional.

From simple two-digit numbers to complex financial figures, mastering this conversion process will enhance your writing precision and meet various formatting requirements across different contexts.

Common Uses of Number-to-Text Conversion

Number-to-text conversion serves multiple purposes across various industries and situations. Understanding these applications helps you recognize when and why accurate conversion matters.

Legal and Financial Documents

Legal contracts frequently require amounts written in both numerical and textual formats. This dual representation prevents fraud and eliminates ambiguity. For example, a check might show “$1,500” numerically and “one thousand five hundred dollars” in text form.

Financial agreements, loan documents, and insurance policies rely heavily on numero a letras conversion to ensure clarity and legal compliance. Banks and financial institutions mandate this practice to reduce errors and disputes.

Academic and Educational Content

Educational materials often present numbers in written form to help students develop reading comprehension and mathematical literacy. Textbooks, worksheets, and assessment materials regularly incorporate number-to-text conversion.

Research papers and academic publications may require specific formatting that includes written numbers for certain values, particularly when following style guides like APA or MLA.

Accessibility and Inclusive Design

Screen readers and assistive technologies perform better when numbers appear in written form. Converting “numero a letras” improves accessibility for visually impaired users and ensures compliance with web accessibility guidelines.

Digital content creators increasingly recognize the importance of inclusive design, making number-to-text conversion a valuable skill for web developers and content managers.

Tools and Resources for Easy Conversion

Modern technology offers numerous solutions for numero a letras conversion, ranging from simple online tools to sophisticated software applications.

Online Conversion Tools

Free web-based converters provide instant results for basic number-to-text conversion needs. These tools typically handle standard numerical ranges and offer multiple language options, including Spanish for true “numero a letras” conversion.

Most online tools support various number formats, including integers, decimals, and currency values. However, accuracy can vary between platforms, making it important to verify results for critical applications.

Software Applications and APIs

Professional applications often include built-in numero a letras functionality. Accounting software, document processors, and financial management systems frequently offer automated conversion features.

Developers can integrate conversion APIs into custom applications, ensuring consistent and accurate number-to-text transformation across different platforms and user interfaces.

Mobile Applications

Smartphone apps provide convenient access to numero a letras conversion tools. These applications often work offline and include additional features like voice input and multiple language support.

Mobile solutions prove particularly useful for professionals who need quick conversions while working remotely or traveling.

Manual Conversion Techniques Explained

Understanding manual conversion methods provides valuable backup knowledge and helps you verify automated results.

Basic Number Structure

Numbers follow predictable patterns that make manual conversion systematic. Learning the fundamental structure of number naming helps you tackle any conversion challenge.

Units (1-9), tens (10-90), hundreds (100-900), and larger place values each follow specific naming conventions. Mastering these patterns enables accurate conversion without external tools.

Handling Complex Numbers

Large numbers require careful attention to place value and proper conjunction usage. Thousands, millions, and billions each have specific formatting rules that affect the final written result.

Decimal numbers present additional challenges, requiring precise placement of decimal indicators and proper fraction representation in text form.

Currency-Specific Conversions

Financial amounts often require special formatting that includes currency denominations and fractional components. Understanding these conventions ensures professional-quality results for business applications.

Different currencies have unique naming patterns and formatting requirements that affect numero a letras conversion accuracy.

Best Practices for Accurate Conversions

Implementing consistent practices improves conversion accuracy and reduces errors in your number-to-text transformations.

Verification Methods

Always double-check conversion results, especially for critical documents or legal applications. Cross-referencing multiple sources helps identify potential errors before they become problems.

Reading converted text aloud can reveal formatting issues or awkward phrasing that might not be immediately apparent when reviewing silently.

Consistency Standards

Establish clear formatting guidelines for your specific use case. Consistent capitalization, punctuation, and spacing create professional-looking results and reduce confusion.

Document your chosen standards to ensure consistency across team members and different projects over time.

Context Considerations

Different contexts may require different conversion approaches. Formal documents might need complete written forms, while informal content could accept abbreviated versions.

Consider your audience and purpose when deciding on conversion style and formatting choices.

Addressing Common Errors and Solutions

Understanding typical conversion mistakes helps you avoid problems and troubleshoot issues when they arise.

Formatting Inconsistencies

Inconsistent capitalization, punctuation, or spacing can undermine the professionalism of your converted text. Establishing clear formatting rules prevents these issues.

Pay attention to hyphenation rules for compound numbers and proper conjunction placement between different place values.

Language-Specific Challenges

Spanish numero a letras conversion includes unique grammar rules and gender agreements that don’t exist in English number conversion. Understanding these linguistic requirements ensures accurate results.

Regional variations in number naming can affect conversion accuracy, making it important to specify your target dialect or region.

Technical Limitations

Automated tools may struggle with very large numbers, unusual formatting, or specialized notation. Recognizing these limitations helps you choose appropriate conversion methods for different situations.

Some tools may not handle negative numbers, scientific notation, or complex fractions properly, requiring manual intervention or alternative approaches.

SEO Optimization for Numero a Letras Content

Creating content around number conversion requires strategic SEO approaches to reach your target audience effectively.

Keyword Integration

Natural integration of “numero a letras” and related terms throughout your content helps search engines understand your topic focus. Include variations like “numbers to letters,” “number conversion,” and “written numbers.”

Long-tail keywords such as “como convertir numeros a letras” or “number to text converter” can capture more specific search intent.

Content Structure

Well-organized content with clear headings and subheadings improves user experience and search engine understanding. Use descriptive headings that include relevant keywords naturally.

Internal linking between related conversion topics helps establish topical authority and improves overall SEO performance.

User Intent Alignment

Understanding why people search for numero a letras information helps you create content that satisfies their specific needs. Some users want quick conversion tools, while others need detailed instruction guides.

Providing multiple content formats (tools, tutorials, examples) within your content addresses different user preferences and search intents.

Frequently Asked Questions

What’s the difference between numero a letras in Spanish and English?

Spanish numero a letras conversion follows different grammar rules, including gender agreements and unique number naming patterns. For example, “veintiuno” (twenty-one) changes to “veintiún” before masculine nouns and “veintiuna” before feminine nouns.

How do I convert decimal numbers to written form?

Decimal numbers require special handling of the decimal point and fractional components. In English, “125.50” becomes “one hundred twenty-five and fifty hundredths” or “one hundred twenty-five point five zero” depending on context.

Are there standard rules for writing very large numbers?

Large numbers follow established patterns using thousands, millions, billions, and beyond. The key is maintaining consistent place value recognition and proper conjunction usage between different magnitude levels.

What’s the best way to handle currency conversion?

Currency amounts typically require both the whole number portion and fractional components written out, such as “one thousand five hundred dollars and twenty-five cents” for $1,500.25.

How can I ensure accuracy when converting numbers manually?

Break complex numbers into smaller components, verify each section individually, then combine them following established grammar rules. Reading the result aloud often reveals errors that visual review might miss.

Transform Your Number Writing Skills Today

Mastering numero a letras conversion enhances your professional writing capabilities and ensures accuracy across various applications. Whether you’re preparing legal documents, creating accessible content, or simply improving your language skills, these techniques provide the foundation for consistent, professional results.

Start practicing with simple numbers and gradually work up to more complex conversions. Combine automated tools with manual verification methods to achieve the highest accuracy levels. Remember that different contexts may require different approaches, so adapt your technique based on your specific needs and audience requirements.

The investment in learning proper numero a letras conversion pays dividends through improved document quality, reduced errors, and enhanced professional credibility. Begin implementing these practices in your current projects and experience the difference that precise number-to-text conversion makes.

Alfred McArthur: A Complete Guide to the Name, Works, and Legacy

Introduction — Meet Alfred McArthur Alfred McArthur is a name that shows up in books, music, and media. People often...

“Duster SUV: Complete Guide to Features, Specs, Safety, and Buying Tips”

Introduction The word Duster brings to mind a simple, sturdy SUV many people trust. This car feels practical and honest....

Keeping It Simple: Why Uncontested Divorce Feels Like a Breath of Autumn Air

The Beauty of Simplicity There’s something undeniably soothing about a crisp autumn morning; the way the cool air clears your...

What is Zivechatz? Full Review, Features, and How to Use It

Introduction — Welcome to Zivechatz and why it matters Zivechatz is a fresh name you might see when looking for...

온도 onuconvert — Easy Temperature Conversion Guide (English)

Introduction: What this guide will do for you This guide helps you understand temperature and how to convert it fast....

Why More Indian Start-ups Prefer Business Setup Dubai UAE for Expansion

When Indian start-ups think about moving beyond home ground, Dubai usually comes up early in the discussion. It is nearby,...

best islamic quotes: simple wisdom for every day

Introduction This article shares calm, clear, and friendly ideas about faith. I wrote this to help you find short reminders....

-

Technology3 years ago

Technology3 years agoIs Camegle Legit Or A Scam?

-

Travel3 years ago

Travel3 years agoNEW ZEALAND VISA FOR ISRAELI AND NORWEGIAN CITIZENS

-

Uncategorized3 years ago

Uncategorized3 years agoAMERICAN VISA FOR NORWEGIAN AND JAPANESE CITIZENS

-

Fashion12 months ago

Fashion12 months agoGoda Perfume Reviews: Is It Worth Your Investment?

-

Health3 years ago

Health3 years agoHealth Benefits Of Watermelon

-

Home Improvement7 months ago

Home Improvement7 months agoArtificial Grass Designs: Perfect Solutions for Urban Backyards

-

Technology3 years ago

Technology3 years agoRNDcoin: Korea’s first blockchain project and a world-class cryptocurrency

-

Fashion2 years ago

Fashion2 years agoBest Essentials Hoodies For Cold Weather